Sticker Shock

Sticker Shock

When you retire, your pharmacy plan is very, very different.

There are a lot of things to consider about retirement. One, of course, is how you will handle your expenses on an essentially fixed income. You’re probably used to paying no more than forty dollars for prescriptions. Depending on what yours are, your costs may go up or down, but if they go up, they can go way up.

I was chided by UFT retirement consultants for complaining about this. They said, correctly, that they had no way of knowing what future expenses may be. I’m sure they do everything they’re trained to do. It might be a good idea, though, if UFT bosses were to get off their pedestals for at least a few moments and extend the training. (They probably won’t, though, and I’ll come back to speculate as to why.)

When I retired, we learned that my wife had a prescription that would cost $300 per month. This was a brand prescription, for which no generic was available. This was an expense we had not foreseen. My wife spoke to her doctor, and he had a nurse call her. The nurse said we could apply to the company for some kind of program that would help with out-of-pocket costs.

I was sceptical. I was pretty sure my income would preclude any sort of help. Nonetheless, we filled out the application, and I faxed it to the drug company. Very shortly thereafter, they sent some kind of coupon to Walgreen’s. Evidently, Express Scripts doesn’t participate in these programs. (Why do we affiliate with a company not doing all it can to help members?) When we went to buy my wife the prescription, there was a high price tag, but it zeroed out and we paid nothing.

Know that these programs are free. You just need to know where to look. There is a company on the net that will hook you up with these programs for $49 a month. If you balk at paying the 49 bucks, they will withdraw your application. These folks are crooks, parasites, preying on Americans desperate to get pharmaceuticals. Information, which most of us haven’t got, and I just stumbled upon, would force them out of business.

That was one problem solved. I later learned, though, that one of my prescriptions, a generic at that, for 90 days, would cost $938.98 at Express Scripts. I learned this during a phone call, and the Express Scripts rep sounded as shocked as I was. At every other pharmacy, it was $968.47, so they did indeed have the best price. There would be no manufacturer programs to help pay for generics.

I took a peek at GoodRX prices to see what I could get with a coupon. It turned out that, rather than the 3700 plus it was going to run my prescription program, I could get a 90-day supply for about $1400. My program says I have to pay 25%, so I figured I’d be able to pay $350 for a three month supply.

I then learned that GoodRX does not work with Medicare pharmacy programs. A younger retiree could’ve done it, but once you’re on a government program, they insist on paying the non-discounted price. While that makes no sense at all, that’s the way it is.

I started looking for prescriptions from Canada. There are a whole lot of Canadian pharmacies on the net. If you look closely, though, you notice that the drugs they sell are not made in Canada, and not even approved for sale in Canada. So the ones made in one country may be far cheaper than those made in another. How do you even know you’re getting real drugs that will help you? Very cursory research suggested you simply do not.

A friend recommended a company that she used to buy veterinary prescriptions. I don’t need help with veterinary prescriptions. My dog’s insurance pays 90% of the cost of his prescriptions. While I was fantasizing about having pharmacy insurance as good as my dog’s, she mentioned to me that the company also sold prescriptions for humans.

The prescription I needed was there, and for 600 bucks, I could buy a three-month supply that was “approved for use in New Zealand.” That sounded better to me than simply, “made in Turkey,” even though it was double the price. I was considering this, but decided to visit my doctor first.

The doctor was shocked when I told him this story. I asked him to write me a paper prescription. I would send it to my niece in Canada and see what she would pay in a brick and mortar pharmacy. How much would it cost me to get drugs that were actually approved for Canadians to use?

The doctor, though, updated my prescription with a different generic he wanted me to try. I scanned it and sent it to my niece. The next day, just for fun, I priced it at Express Scripts. They wanted $639.16 for it. Pretty high, but not as high as the one I’d been using. Furthermore, this was a moderate improvement over local pharmacies, which wanted $639.23. I could save over two cents a month if I used my UFT-recommended pharmacy.

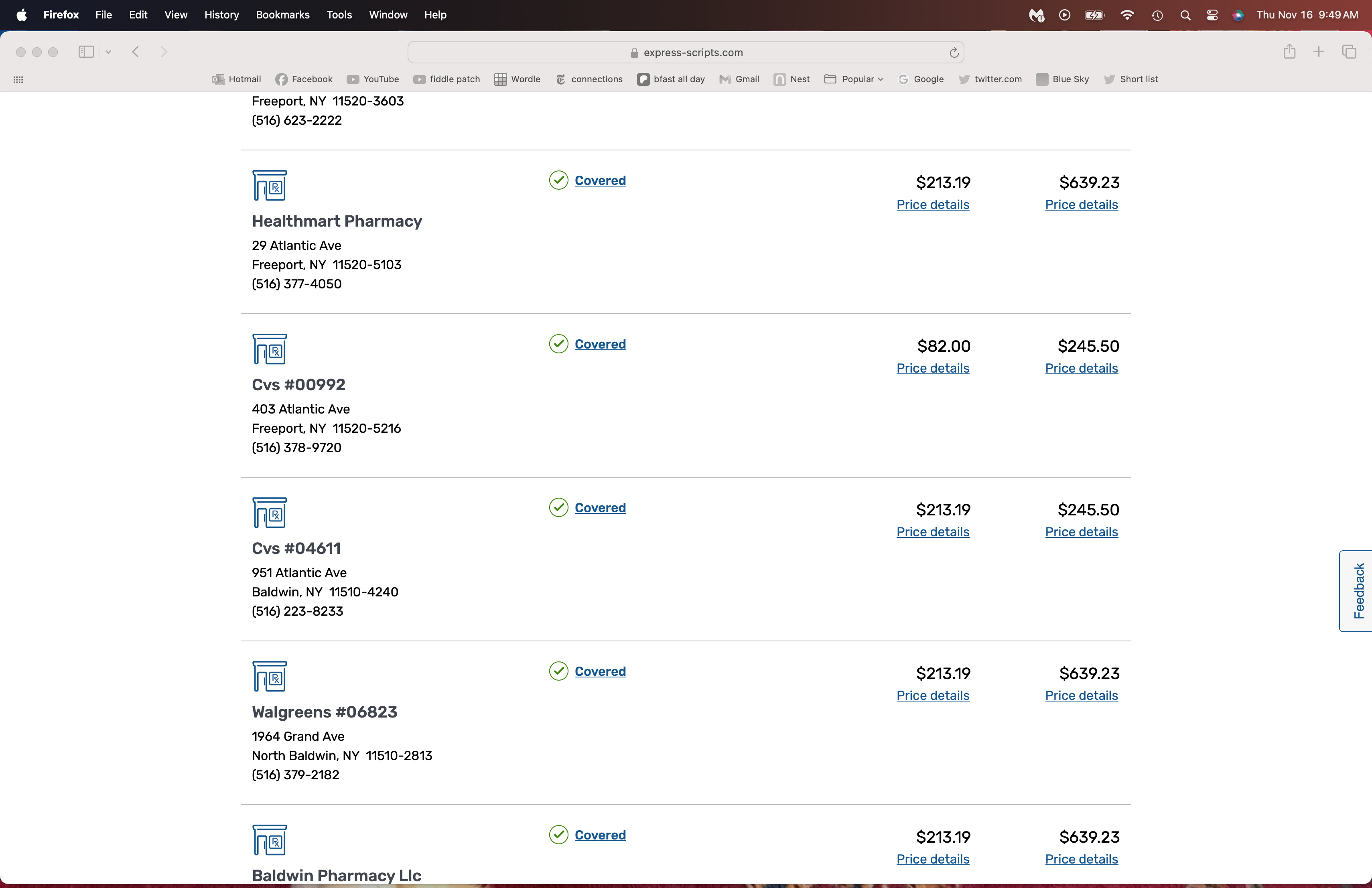

As I scrolled down, though, I got a surprise, though. Take a look at these prices:

The CVS near my house was offering it for $245.50 for a three-month supply. I was sure that was too good to be true. I called CVS to verify, but they said they couldn’t do so until they got the prescription. I asked my doctor to phone it in. The next day, I paid them $245.50 and got the meds. I hope they work as well as the others. My doctor thinks they will.

Here’s the thing—UFT bosses can’t be bothered helping with things like member expenses. They’re out there working to dump retirees into a Medicare Advantage plan, with copays for everything. They boast of an $1800 limit, but with real medicare you pay a $240 deductible, and that’s it for doctor visits. Mulgrew and his Unity cult want us to pay up to 1500 more a year, each, and that’s before we even look at hospital care.

The fact is, retirees may have far more expenses than in-service members already. UFT-Unity’s willingness to throw us to the dogs, after decades of service and union dues, is beyond disgraceful.

If they actually wanted to help, they’d initiate programs to do so. They’d help us connect with programs to find affordable prescriptions. They’d research places we could buy drugs cheaper. They’d arrange for retirement consultants to warn us of actual prices we might encounter, should we choose to share our prescription info with them.

Instead, they’re on a mission to degrade our health care, and dump us into a corporate program with every incentive to deny us as much care as they possibly can. And if you’re in-service, they’re looking to place you in a program that will cost Eric Adams 10% less. They will tell you that it will be as good as better, but it’s pretty hard to see how that could be true.

They lied to us, saying every doctor that took Medicare would take their Advantage plan. They’re lying to rank and file as well.

If you want lower-quality, more expensive health care, vote for UFT Unity. If not, check out the opposition. If you’re a retiree, you can vote for me with Retiree Advocate. If you’re rank and file, elections are coming up next year.

I’d cast a vote for my dog before I’d cast one for UFT Unity. And you probably would too.

I don't and can't defend the retiree prescription plan but share my experience in the hope that it might be useful to someone.

I take one expensive medication that is covered by Medicare but whose annual expense forces me into the dreaded Medicare "donut-hole" that exposes me to a large out-of-pocket payment. Express-Scripts did refer me to a patient assistance program that has covered those out-of-pocket payments for the last two years. The assistance is income-tested but seemed to be somewhat flexible and the medication has to be for a "covered" disease.

At any rate, here's the link to Patient Assistance Foundation Co-Pay Relief Fund which folks should always check out: https://copays.org.

I take another expensive medication for which I get patient assistance support through Healthwell Foundation, again, worth a try: https://www.healthwellfoundation.org/.

Yes, my dog also would do a better job. Yes, she too has better insurance that pays 90 percent of all costs. I should write to Mulgrew and say I should have insurance as good as my dog’s.